Last week, the U.S. Departments of Labor and Treasury issued a Joint Notice requiring the extension of certain benefit plan deadlines for individuals affected by Hurricanes Helene and Milton and Tropical Storm Helene.[1] The deadline extensions echo relief issued during the COVID-19 pandemic, but apply to a more limited group of individuals. The relief is intended to address challenges that affected plan participants and beneficiaries may face in meeting certain plan deadlines in order to access employee benefits.

Pursuant to the Joint Notice, benefit plans subject to ERISA or the Internal Revenue Code are required to disregard a defined “Relief Period” when determining certain plan deadlines applicable to participants, beneficiaries, COBRA qualified beneficiaries and claimants affected by the disasters.[2] Below we answer questions related to the scope of the relief, and offer recommendations for plan sponsors and administrators regarding implementation of the deadline extensions.

Who is Entitled to the Deadline Relief?

The relief applies to pension and welfare (including group health) plan participants, beneficiaries, COBRA qualified beneficiaries and claimants directly affected by the disasters. According to the Joint Notice, an individual was directly affected if they resided, lived, or worked in one of the disaster areas at the time of the hurricane or tropical storm, or their benefit coverage was under a plan that was directly affected by the disasters. The disaster areas include counties and tribal areas in Florida, Georgia, North Carolina, South Carolina, Tennessee and Virginia that have been or are later designated by the Federal Emergency Management Agency (FEMA) as disaster areas eligible for Individual Assistance due to Hurricanes Helene or Milton or Tropical Storm Helene.[3]

Which Plan Deadlines Are Extended?

The relief applies to benefit plan deadlines related to:

- HIPAA special enrollment,

- COBRA elections, premium payments, and notice of qualifying events and Social Security disability determinations, and

- the filing of claims and appeals under pension and welfare plans, as well as requests for external review under group health plans.

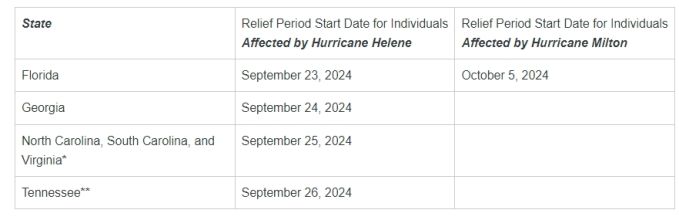

What is the Duration of the Relief Period?

The Relief Period ends on May 1, 2025 for all affected individuals, but starts on different dates depending on which disaster affected the individual, as follows:

*or Tropical Storm Helene

**Tropical Storm Helene

What Exactly Does the Joint Notice Require?

The applicable Relief Period must be disregarded when determining the timeliness of an affected individual’s: (i) request for special enrollment in a group health plan (e.g., upon marriage, or birth or adoption of a child); (ii) COBRA election, premium payment, or notice of qualifying event or disability; or (iii) filing of a claim, appeal or request for external review (or perfection of a request for review).

For example, if an affected individual, who worked in one of the disaster areas in North Carolina at the time of Hurricane Helene, lost group health coverage and is provided with a COBRA election notice on December 1, 2024, the individual would have until 60 days after May 1, 2025 to elect COBRA coverage, since the Relief Period (September 25, 2024, to May 1, 2025) is disregarded in determining the COBRA election deadline.

Similarly, if an affected individual, who lived in one of the disaster areas in Tennessee at the time of Tropical Storm Helene, was notified of an adverse benefit determination from a group health plan on August 28, 2024, the individual would have until 151 days after May 1, 2025 to file an appeal (within the required 180-day appeal period), since the Relief Period (September 26, 2024, to May 1, 2025) is disregarded in determining the appeal deadline.

Is There Any Relief for Plan Sponsors and Administrators?

The Joint Notice includes limited relief for plan sponsors and administrators directly affected by the disasters (e.g., the plan’s or its sponsoring employer’s principal place of business was located in one of the disaster areas). The only relief afforded to these plans under the Joint Notice is that the applicable Relief Period is disregarded when determining the date by which the plan must provide a COBRA election notice.

However, in the related EBSA Disaster Relief Notice (2024-01), the DOL provides plan sponsors and fiduciaries additional time to meet their obligations under Title I of ERISA as a result of the disasters. Pursuant to the Notice, responsible fiduciaries will not be in violation of ERISA if they fail to timely furnish a notice or other document that must be furnished to participants, beneficiaries and other persons during the applicable Relief Period, provided that the fiduciary acts in good faith and does so as soon as administratively practicable under the circumstances. As an example, DOL states that good faith acts include the use of electronic communications with respect to individuals who the plan fiduciary reasonably believes have effective access to electronic communications, including email, text messages, and continuous access websites.[4]

Implementation Action Items

The Joint Notice does not include any specific requirements regarding implementation of the deadline relief. However, the spirit of the guidance suggests that plan sponsors and administrators should promptly notify individuals of the relief so that they can take advantage of it, particularly if the plan covers (or covered) individuals who resided, lived, or worked in the disaster areas at the time of the hurricanes or tropical storm. Plan sponsors and administrators will need to consider to whom notices should be sent and by what means, taking into account the geographical composition of the employer’s workforce (as well as dependents, retirees and COBRA qualified beneficiaries) or the plan’s coverage area in the case of a multiemployer plan. Consideration also should be given to whether targeted notices may be appropriate in some circumstances, and whether there are situations where past actions have to be un-done (such as termination of COBRA coverage due to non-payment, or denial of a late special enrollment request).

***

Plan sponsors and administrators will be well-served to communicate the relief as soon as possible, particularly given the retroactive start date of the Relief Period. In addition, plan personnel should be trained to respond to requests for deadline extensions. It also will be important to ensure that insurers, claims administrators, and other third-party vendors such as COBRA administrators are acting in compliance with the Joint Notice, and inquire about their intended communication efforts.

[1] The U.S. Department of Labor also issued FAQs that include guidance related to the deadline relief.

[2] As stated in the Joint Notice, the U.S. Department of Health and Human Services (HHS) concurs with the relief and encourages plan sponsors of non-federal governmental plans and health insurance issuers offering group and individual health insurance coverage to apply similar relief.

[3] A list of areas that have been designated as eligible for Individual Assistance can be found on FEMA’s website at www.fema.gov/disasters.

[4] The Disaster Relief Notice includes additional relief for plan sponsors and fiduciaries related to the processing of plan loans and distributions, forwarding participant contributions and loan repayments, furnishing blackout notices, and the filing of Forms 5500 and M-1s. The Notice also requests that plan fiduciaries make reasonable accommodations to prevent the loss of employees’ benefits or undue delay in benefit payments, and to minimize the possibility of lost benefits due to failures to comply with deadlines.