June 2023 Interest Rates for GRATs, Sales to Defective Grantor Trusts, Intra-Family Loans and Split-Interest Charitable Trusts

The June Section 7520 rate for use in estate planning techniques such as CRTs, CLTs, QPRTs and GRATs is 4.2%, a slight decrease from the May rate of 4.4%. The June applicable federal rate (“AFR”) for use with a sale to a defective grantor trust or infra-family loan with a note having a duration of:

- 3 years of less (the short-term rate, compounded annually) is 4.43%, up from 4.30% in May.

- 3 years to 9 years (the mid-term rate, compounded annually) is 3.56%, down from 3.57% in May.

- 9 years or more (the long-term rate, compounded annually) is 3.79%, up from 3.72% in May.

IRS Data Book Released for Fiscal Year 2022

The IRS released its 2022 Fiscal Year Data Book reporting agency activity. 2022 Fiscal Year (October 1, 2021 – September 30, 2022) highlights:

- The IRS collected $33,355,276,000 in estate and gift taxes for FY 2022 (up $5,309,537,000 from FY 2021)

- $28,909,393,000 collected from estate tax (up $5,484,367,000 from FY 2021)

- California decedents paid the most estate tax in FY 2022 ($5,778,261,000)

- West Virginia decedents paid the least estate tax in FY 2022 ($3,674,000)

- $4,445,883,000 collected from gift tax (down $173,830,000 from FY 2021)

- California residents paid the most gift tax in FY 2022 ($669,690,000)

- Alaska residents paid the least gift tax in FY 2022 ($98,000)

- $28,909,393,000 collected from estate tax (up $5,484,367,000 from FY 2021)

- There were 27,088,000 estate tax returns filed in FY 2022 (down 138,500 filings from FY 2021)

- California filed the most estate tax returns for FY 2022 (4,343,000)

- Alaska filed the least estate tax returns for FY 2022 (36,000)

- There were 270,142,000 gift tax returns filed in FY 2022 (down 119,120 filings from FY 2021)

- California had the most gift tax returns filed for FY 2022 (34,808,000)

- Alaska had the least amount of gift tax returns filed for FY 2022 (463,000)

- In FY 2022, the IRS closed 1,398 estate tax return audits, resulting in $1,764,755,000 in recommended additional tax.

- of the 1,398 estate tax return audits closed, 59 of the taxpayers did not agree with the IRS examiners findings, resulting in an unagreed recommended additional tax of $1,138,478,000.

- In FY 2022, the IRS closed 904 gift tax audits, resulting in $761,867,000 in recommended additional tax.

- of the 904 gift tax return audits closed, 94 of the taxpayers did not agree with the IRS examiners findings, resulting in an unagreed recommended additional tax of $418,744,000.

- The IRS assessed $476,782,000 in civil penalties for estate and gift tax returns and abated $333,082,000 in civil penalties for estate and gift tax returns.

PLR 2023150002

S Corporation's (the "Corporation") shares were transferred to a Trust that was eligible to elect qualified subchapter S trust (QSST) treatment under Section 1361(d) of the Internal Revenue Code of 1986, as amended (the "Code"). The beneficiaries of the Trust failed to make timely QSST elections and therefore, the Corporation's S election terminated. The Corporation represented that they have filed consistently with the treatment as an S Corporation since the transfer of the shares into the Trust and that it relied on its accounting firm to make the QSST election. The IRS found that the termination of the Corporation's S election was inadvertent within the meaning of Section 1362(f) of the Code. Pursuant to Section 1362(f), the Corporation would continue to be treated as an S Corporation from the date of the transfer of the shares and thereafter, provided that the Corporations election was valid and not otherwise terminated under Section 1363(d) of the Code.

Wrzesinkski v. United States, No. 2:22-cv-03568, (E.D. Pa. Mar 7, 2023)

This is a case of first impression dealing with Form 3520 penalties for foreign gifts. Krzysztof Wrzesinski was born and raised in Poland. He immigrated to the United States at 19 and began working in public service as a police officer. In 2010, his mother, a citizen and resident of Poland, won the Polish lottery and decided to gift to Krzysztof $830,000 over the course of 2010 and 2011. Krzysztof consulted his tax advisor about whether there were any tax implications from receiving the gifts from his mother. His tax advisor told him that he did not need to file any forms with his tax return and that the gifts he received were exempt from gross income. Preparing to do some gifting of his own to his godson in Poland, Krzysztof thought he may have reporting responsibilities when gifting to persons abroad. Thus, Krzysztof did a quick search online which led him to various articles about the reporting requirements of U.S. individuals when receiving a gift from foreign persons, as opposed to U.S. individuals sending gifts to foreign persons. In an attempt to correct his obvious failure to report the gifts from his mother, Krzysztof contacted an attorney to help him file late Forms 3520 (the "Annual Return to Report Transactions with Foreign Trusts and receipt of Certain Foreign Gifts") for the 2010 and 2011 gifts. Krzysztof utilized the DIISP (Delinquent International Information Return Submission Procedures) and attached statements indicating he relied on erroneous tax advice and therefore penalties should be abated. While the gifts were exempt from gross income, Krzysztof was hit with penalties in the amount of $87,500 and $120,000 for failing to file Form 3520 for 2010 and 2011. Krzysztof appealed the penalties on the basis of reasonable reliance and the Appeals officer agreed to abate $166,000 of the total $207,500 penalty. This left Krzysztof with $41,500 (or 5% of the total gifts) to pay in penalties. Krzysztof paid the penalty even though he still disagreed with the IRS and filed claims for refund in March 2022, which the IRS then denied. The IRS, in denying Krzysztof's claims for refund, took the position that the claims did not establish reasonable cause. In turn, Krzysztof initiated a refund suit in federal district court in September 2022. In a surprising turn of events, the IRS agreed to fully concede the case in favor of Krzysztof before they even filed an answer to his initial complaint.

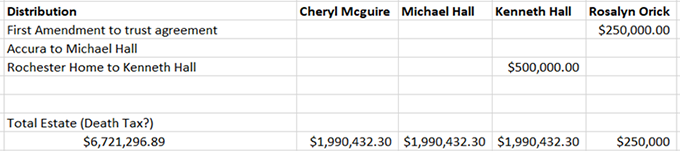

McGuire v. Hall (In re Gregory Hall Tr.), Nos. 361528, 362467, 2023 Mich. App. LEXIS 1866 (ct. app. Mar. 16, 2023)

In 1993, Gregory Hall created a revocable trust that he amended and restated in 2005 (the "2005 Amendment"). The 2005 Amendment provided that the residue would be divided equally between his three children: Kenneth, Cheryl and Michael. Additionally, the 2005 Amendment stated that Gregory could, during his lifetime, by an instrument in writing delivered to the Trustee modify, alter, amend or revoke this trust, in whole or in part.

In late 2014, Gregory conveyed his house to Kenneth. At the time of the conveyance, the house was valued at $500,000. On January 18, 2016, Gregory made a spreadsheet that showed his overall estate (as of October 13, 2017) to be $6,721,296.89. It also reflected a specific bequest to Rosalyn Orick of $250,000, Kenneth receiving the house valued at $500,000, and each of the children's columns showed a total distribution of $1,990,432.30.

Gregory died on April 11, 2018, and Kenneth, Cheryl and Michael become co-Trustees of the trust. Cheryl and Michael petitioned the Court for limited supervision of the trust and approval of a proposed plan of distribution that treated the conveyance of the house as an advancement of $500,000 to Kenneth. Kenneth argued that the conveyance of the house was a gift and therefore he was still entitled to one-third of the residue.

To determine whether the transfer of the house was an advancement to Kenneth, the parties sought to discover communications between Kenneth and Gregory. The Trial court entered orders directing Kenneth and his wife, Beth, to produce their electronic devices for retrieval and preservation of ESI. Kenneth and his wife, Beth, ignored the Trial Courts orders. Specifically, Beth exchanged her iPhone for a new one and all of the e-mails on Gregory's computer from 2012-2013 were deleted. Oddly, when Kenneth received a discovery request to produce electronic communications relevant to the transfer of the house, he managed to produce only three emails that had been sent to Gregory but were no longer on Gregory's computer because they had been mysteriously deleted.

After a tumultuous discovery process, the Court found in favor of Cheryl and Michael that the house was an advancement to Kenneth and did so only as a discovery sanction and not based on legal merit. For two and half years, Kenneth continuously ignored the Court's orders regarding discovery and the Court, after issuing less severe financial sanctions, finally found that Kenneth's discovery violations were "so persistent and egregious" that a default against him was the only appropriate penalty. Kenneth appealed the ruling, and the Appeals Court of Michigan upheld the Trial Court's ruling.

While the default judgement ultimately resolved the dispute, the question of fact remained. In a ruling for summary disposition filed by Cheryl and Michael, the probate court found that the spreadsheets created by Gregory met the statutory definition of a contemporaneous writing pursuant to the Michigan statutes as applied to trusts and met the definition of an amendment to the trust pursuant to the Michigan statutes and Article IV of the trust.